Before the Battlefield: Industrial Power, Supply Chains and Strategic Resilience

Key Takeaways

Supply chain resilience is increasingly part of global power competition.

Major powers are aiming to increase critical mineral supply chain resilience through diversification and stockpiles.

Emerging economies are re-emerging as part of the supply chain strategy.

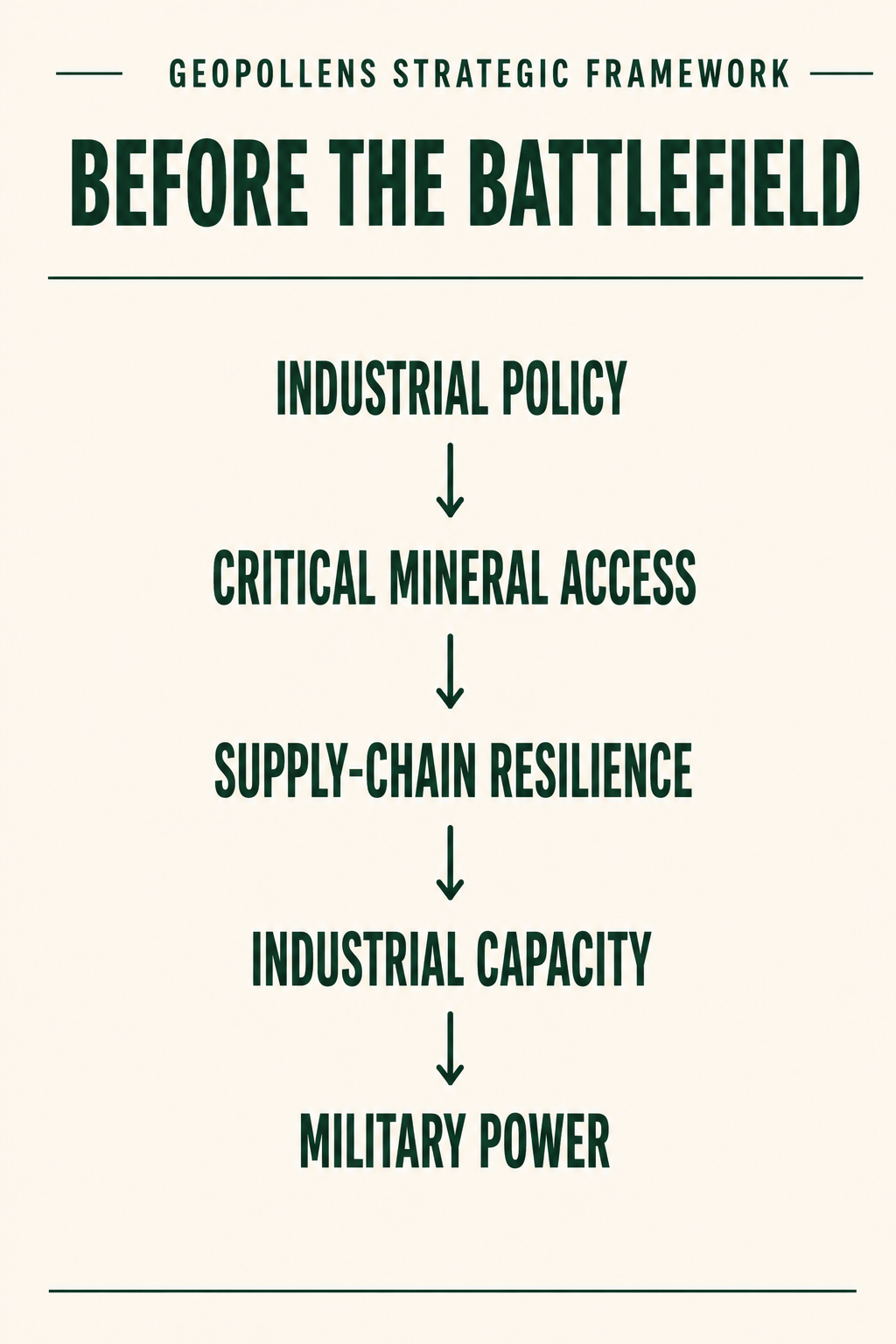

Modern conflict is reinforcing the importance of industrial and logistical infrastructure that sustains military power.

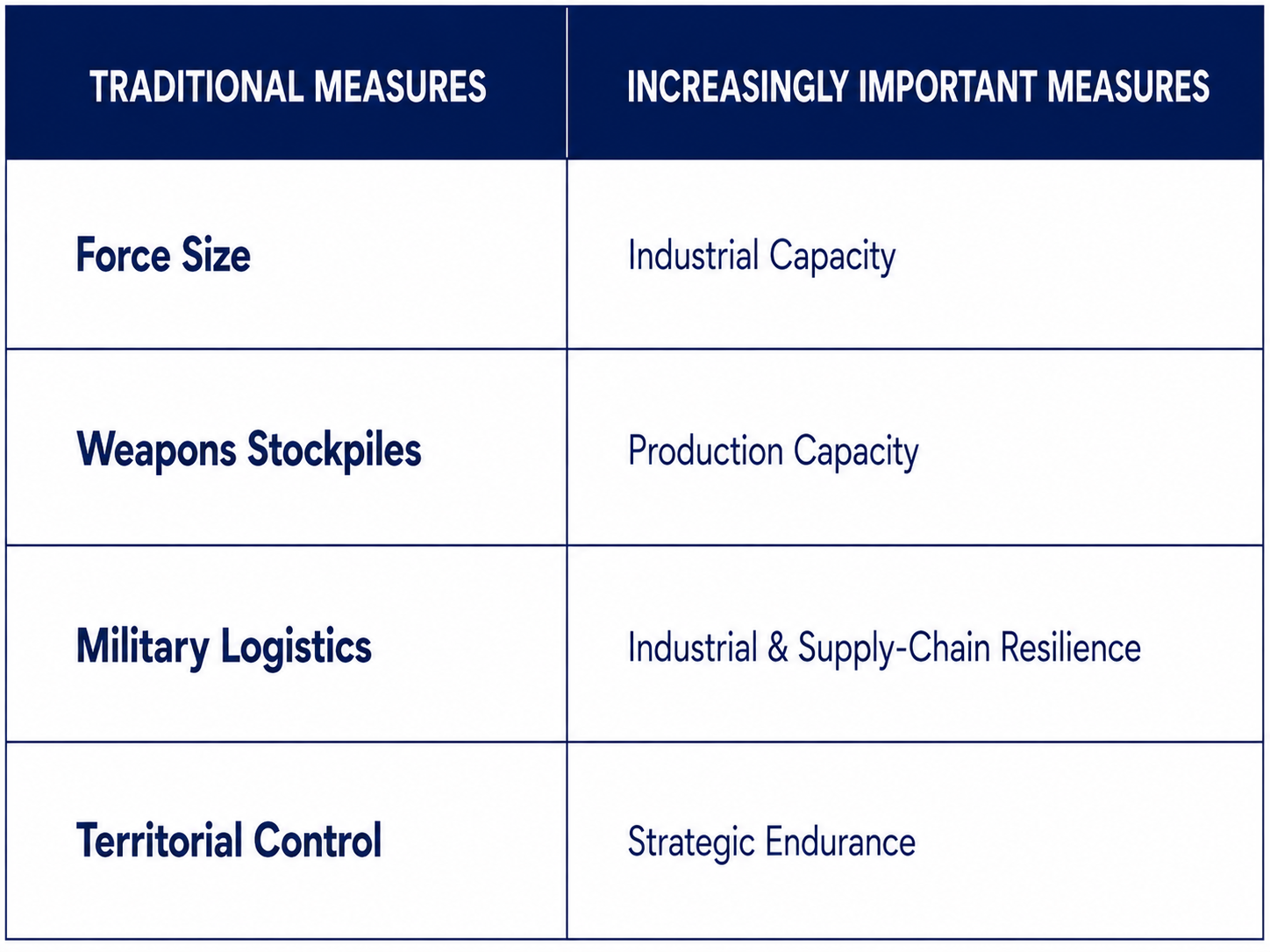

Military power has traditionally been measured in conventional terms such as force size and military and naval capacity. More recently, a shift in focus toward the ability to obtain resources to produce, sustain, and replace capability is becoming more prominent. Competition is not only hard power and armed forces but also ensuring that countries have the industrial base to maintain capacity. Strategic competition is becoming noticeably about resources, supply chains, manufacturing, and energy security that underpin military power.

Industrial capability has always been linked to military power. Globalisation has resulted in decades of dispersed supply chains, with certain countries now dominating specific resources through economic efficiency and industrial policy. Governments that once believed they had the ability to access strategic supply chains are now reassessing their exposure and the impact on strategic resilience. Competition is realigning and not solely focused on hard power but increasingly on resources, capacity, and supply chains that are needed for economic growth and to sustain military capacity. Securing supply chains is re-emerging as being intertwined with national security.

Modern defence systems are dependent on specialised materials used in advanced technology. The manufacturing of missiles, drones, satellites, aircraft, and communications relies on supply chains, often sourced from countries that may not be strategic partners. Inputs such as critical minerals, batteries, and semiconductors have become vital to sustain military capacity. With certain countries dominating these inputs, any disruption to a single component could affect both the economy and defence production. As some countries have specialised in specific inputs or increasingly control supply chains, governments are progressively considering access to inputs as a strategic priority.

The re-focus on diversification and supply chains among major powers is notable in strategic documents. The 2025 U.S. National Security Strategy is direct in noting that “...we want to ensure our continued access to key strategic locations” and to end “threats against our supply chains that risk U.S. access to critical resources, including minerals and rare earth elements.” More recently, at the G7 summit, the message was similar. The G7 released a statement outlining the Critical Mineral Action Plan, stating that they “ recognise the strategic role of critical minerals value chains for our countries’ economic prosperity and security, including our digital and energy sectors.” Such statements highlight that the re-focus is becoming a priority and one that is multi-layered.

Both the NSS document and G7 statement indicate that it is not only about access to supply chains. By reducing critical dependencies, such countries will be less exposed to export measures or retaliatory restrictions, which would impact dual-use inputs important for economic and national security. However, diversification will require significant investment in industrial capacity and potentially forming agreements with emerging countries to secure access to critical minerals. Not only that, but there is the intention to develop domestic markets in order to create stockpiling systems where strategic partners can share information and increase diversification. The urgency is evident in specific objectives such as the G7 aiming to reduce dependence on a singular supplier of rare earths and permanent magnets to under 60% by 2030. Currently China controls approximately 90% of the global rare earth processing and permanent magnet production, highlighting the dominance and dependence on one supplier.

China’s restrictions on shipments of rare earths after trade tension with the U.S. in 2025 accelerated diversification. At one point, Chinese rare earth exports were down by 50%, with a year-on-year basis at 74% in May 2025. The restrictions created a supply choke point that had impacts across defence and industrial supply chains, with the minerals used in renewable energy components, semiconductors, batteries, and refining processes. Since the restrictions, the U.S. has made efforts to invest in new projects financing mining, processing, and magnet manufacturing domestically and with partners such as Australia, Brazil, and Saudi Arabia. More recently, emerging economies in Africa have reemerged as potential partners.

Following the G7 summit, a preliminary agreement between the U.S. and Kenya for access to mineral deposits was announced. With earlier estimates of USD 64 billion of rare earth deposits in Mrima Hill, the agreement signals a U.S. pivot to Africa, where China is currently the main processor and supplier of minerals. The agreement will be unlike previous models where raw materials were extracted and exported, with Kenya set to be involved in processing. The announcement after the G7 discussions demonstrates the priority the U.S. places on critical supply chains for its economic and national security.

Supply chains are increasingly becoming strategic infrastructure required to sustain military and economic capability. Disruption to supply chains can have a rapid impact, as seen by the automotive industry that suspended, shut down, or faced severe impacts shortly after the restrictions were announced. For the defence industry, rare earths are required for jets, submarines, radar systems, missiles, and unmanned aerial vehicles, for example. Maintaining production at a time when China is estimated to be manufacturing munitions, advanced weapons, and equipment to that of the U.S. adds another layer of pressure to sustain supply chains. It highlights that defence supply chains can be targeted and disrupted with relative ease and have almost an immediate impact. The shift in policy of supply chain diversification and stockpiling is aiming to build resilience against the disruption of this strategic infrastructure, reflecting the disruption caused by drone strikes on defence-related infrastructure in Russia.

Ukraine has targeted industrial and logistical infrastructure that sustain Russian military capacity to reduce its ability on the front line. The asymmetrical tactic has targeted refineries, energy revenue, logistical hubs, military production, and naval and air bases. Rather than solely focus on territorial gains, Ukraine has targeted systems, logistics, and production that sustain Russia’s ability to conduct its campaign. With reports of Russian advancement on the front line steadily decreasing compared to previous years, the Institute for the Study of War assessed the Russian military had advanced 16.04 square kilometers per day in June 2025, compared to 1.01 square kilometers per day in June 2026. Ukrainian strikes demonstrate that targeting industrial infrastructure remains an important strategic objective. Critical infrastructure has always been significant; however, what is re-emerging is not only the importance of conventional force and territorial gains but also the resilience of systems that support it.

Assessment

Military power and force projection are not solely about conventional capability. Globalisation created interdependence; however, some emerging economies developed dominance over critical mineral supply chains. The current focus is not on a state’s ability to only access resources but also on maintaining the capacity to manufacture, create stockpiles, and build supply chain resilience to avoid disruption. A state’s strength may also be calculated on its ability to achieve these supply chain objectives. Infrastructure has been targeted during conflict; however, supply chain competition is now occurring prior to conflict. States may now be assessing their ability to create resilience across multiple support systems in order to have the capacity to sustain competition.

What to Watch

Investment and expansion of domestic critical mineral infrastructure.

Asian, U.S., and G7 critical mineral agreements with emerging economies, particularly Africa, to expand mining, processing, and refining capacity.

Data indicating growth in strategic stockpiles.

Increased protection of critical infrastructure, ports, energy, rail, and industrial facilities.

U.S. pressure to monitor foreign ports in the Western Hemisphere.

Continued targeting of industrial military infrastructure in the Ukraine-Russia conflict.

Sources

Primary Sources

White House. 2025 National Security Strategyhttps://www.whitehouse.gov/wp-content/uploads/2025/12/2025-National-Security-Strategy.pdf

Government of Canada. G7 Leaders' Declaration on Securing Supply Chains for Critical Mineralshttps://www.pm.gc.ca/en/news/statements/2026/06/17/g7-leaders-declaration-securing-supply-chains-critical-minerals

News Reporting

Reuters. G7 Sets Up Critical Minerals Alliance Crisis Platformhttps://www.reuters.com/world/europe/g7-sets-up-critical-minerals-alliance-crisis-platform-2026-06-17/

Reuters. China's Rare Earth Magnet Shipments Halve in May Due to Export Curbshttps://www.reuters.com/business/autos-transportation/chinas-rare-earth-magnet-shipments-halve-may-due-export-curbs-2025-06-20/

Reuters. U.S. Pushes Quicker Action on Reducing Reliance on China for Rare Earthshttps://www.reuters.com/business/energy/us-push-quicker-action-reducing-reliance-china-rare-earths-2026-01-11/

Reuters. Kenya-U.S. Close Critical Minerals Dealhttps://www.reuters.com/world/africa/kenya-us-close-critical-minerals-deal-ruto-says-2026-06-17/

Reuters. Auto Companies Face Shortages Due to China's Rare Earth Restrictionshttps://www.reuters.com/business/autos-transportation/auto-companies-face-shortages-due-chinas-rare-earth-restrictions-2025-06-05/

Strategic Analysis

CSIS. Rare Earth Export Restrictions One Year Laterhttps://www.csis.org/analysis/rare-earth-export-restrictions-one-year-later

CSIS. China's New Rare Earth and Magnet Restrictions Threaten U.S. Defense Supply Chainshttps://www.csis.org/analysis/chinas-new-rare-earth-and-magnet-restrictions-threaten-us-defense-supply-chains

Regional Reporting

Business Insider Africa. U.S. Edges Out China in Kenya with Preliminary Deal to Control US$624 Billion in Rare Earth Depositshttps://africa.businessinsider.com/local/markets/us-edges-out-china-in-kenya-with-preliminary-deal-to-control-dollar624-billion/e08tmmr

Conflict Assessment

Institute for the Study of War. Russian Offensive Campaign Assessment – 1 July 2026https://understandingwar.org/research/russia-ukraine/russian-offensive-campaign-assessment-july-1-2026/