Strategic Resources: Critical Mineral Diversification and Emerging Markets

Key Takeaways

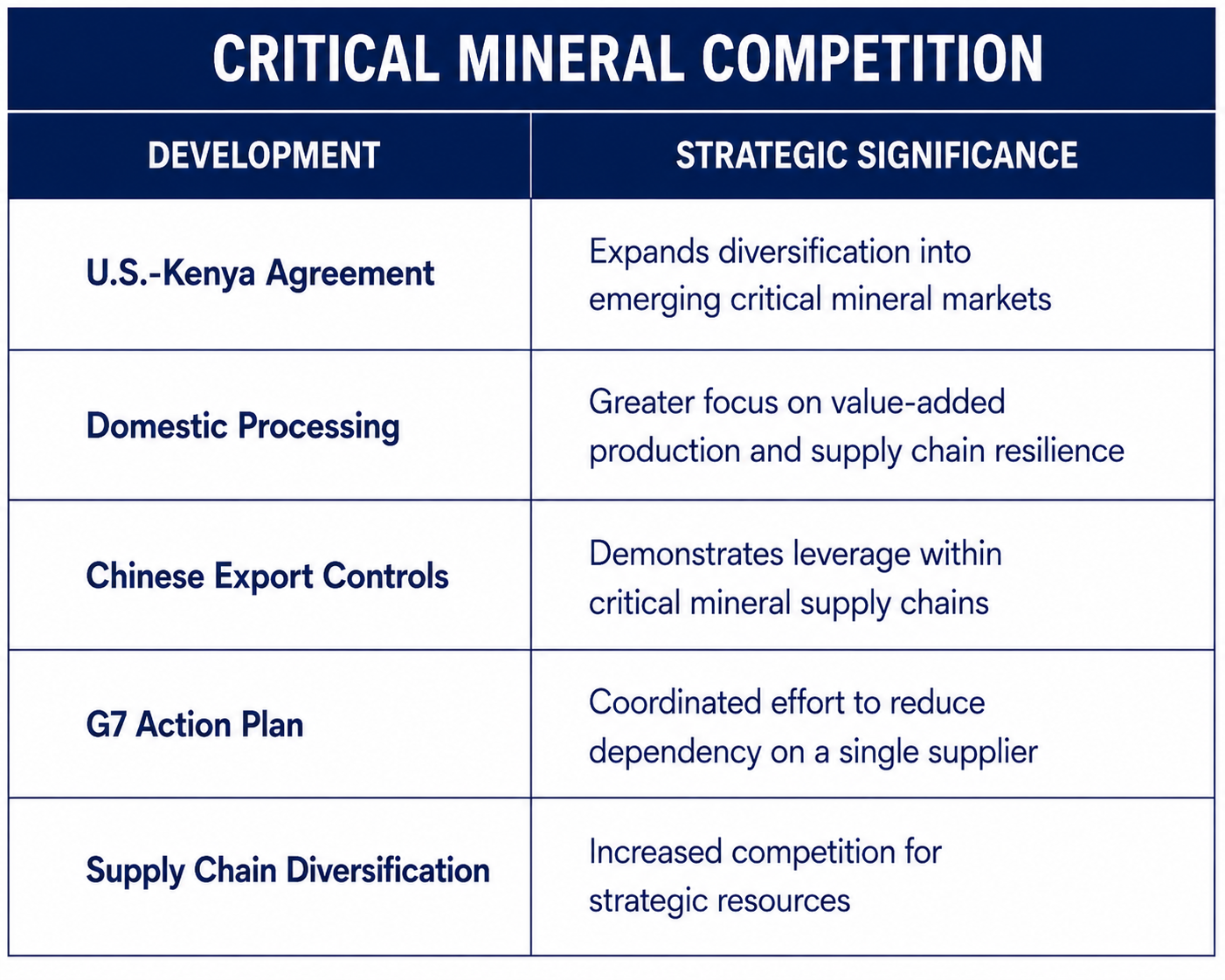

The U.S.-Kenya critical mineral agreement indicates efforts at diversification in emerging markets to reduce dependency.

China’s dominance of critical mineral markets has led to the U.S. and G7 policy shifts towards diversification.

China has engaged in reciprocal control and restriction measures in response to U.S. sanctions as leverage in competition for strategic resources.

The recent announcement of a U.S.-Kenya critical minerals agreement suggests a continuation of U.S. policy to diversify and secure supply chains. The agreement comes after an invitation in April 2026 for expressions of interest to attract bids for rare earths at Mrima Hill. Rather than export minerals, Kenyan President Ruto has stated that processing will be done domestically.

The details surrounding the deal are unknown other than it will likely include rare earths and strategic minerals. Kenya is known to have an array of mineral deposits such as copper, graphite, lithium, nickel, and niobium. Rare earths and minerals have strategic value and widespread use in defence systems, aerospace, batteries, energy storage, power grids, and infrastructure. The move reflects a broader shift in how states view critical minerals, not as commodities but as strategic resources linked with the economy and national security.

The agreement comes as China has previously placed restrictions on critical mineral exports. In April 2025, China implemented controls on critical mineral exports. Many of these minerals are used in defence and military sectors, advanced technology, and energy transition industries, as well as electronics and communications. China’s dominant role in the value chain is evident, as it is responsible for 60% of global mined production of rare-earth magnets and 91% of global refined output. China announced a second round of controls in October 2025, and although they were suspended in November 2025 for one year, the potential risk was apparent. The International Energy Agency estimated that the combination of restrictions would have had an annual downstream global impact on countries outside China of USD 6.5 trillion. While industries such as the automotive sector were highlighted as more significant, it was the U.S. and Europe that were most exposed, with losses estimated at USD 1.5 trillion each. The calculated losses may indicate why critical supply chains have gained prominence recently.

The U.S. has indicated its position on critical minerals with national security in the release of the 2025 National Security Strategy (NSS). Diversification and maintaining secure and reliable supply chains are policy objectives, with the NSS stating that Africa is an “…immediate area for U.S. investment…,” which includes “…the energy sector and critical mineral development.” It is difficult to assess how much the April 2025 Chinese restrictions on critical minerals influenced the NSS. However, the timeframes could indicate that reducing U.S. reliance on Chinese supply chains may have gained prominence after China implemented the controls. Along with the nickel agreement with Indonesia, the U.S. has made efforts to secure alternative sources for strategic minerals and has now turned toward Kenya. The recent agreements are not only U.S. efforts in supply chain resilience but may also be part of a broader approach by partners.

The recent Group of Seven (G7) summit resulted in leaders releasing another joint statement on critical minerals. In June 2025 the G7 issued a declaration with a minerals action plan that, similar to the NSS, highlighted the need for diversification, supply chain resilience, and the links between critical minerals, national security, and economic security. Although China is not mentioned, the G7 explicitly refers to reducing dependence on a single non-member supplier of rare earths and magnets to under 60% by 2030 and eventually to under 50%. Diversification could be challenging to achieve in the immediate future given Japan's experience. For over a decade, Japan has made efforts to reduce its dependence on Chinese supply chains through partnerships, investments, and technology development. Despite this, in 2024 Japan remained the largest importer of Chinese rare-earth metals. It highlights that diversification requires long-term policy and investment.

China’s export restrictions led to shortages of rare earths in the European auto industry, causing some manufacturers to suspend outputs and a statement by the European Union Commissioner for Industrial Strategy saying Europe must decrease its dependency, especially on China. The timeline of the G7 declarations highlights that for the past year the concern about critical mineral supply chains has not gone unnoticed; however, the policy appears to have also drawn a response.

China’s response may be in part to the G7 action plan given the timing and as a continuation of recent U.S. measures. According to Reuters, China has added 10 entities to its export control list, including the Pentagon-backed MP Materials. The Chinese decision bans dual-use exports to named firms in an effort to adhere to non-proliferation obligations and as a matter of national security. It is reported that the measures are mostly symbolic, as the listed companies have U.S. defence ties and are likely to be conducting business with China. Added in a separate announcement by the Chinese Finance Ministry was a ban on purchases from 46 U.S. companies, including Lockheed Martin, Raytheon, and General Dynamics.

The Chinese response may be part of an ongoing strategic competition with the U.S. Recently, the U.S. Defense Department designated several tech companies to a list with ties to the Chinese military, barring these companies from U.S. contracts. It is too early to assess the impacts of these measures; however, both China and the U.S. appear to be signalling that economic resources and critical minerals are being used as leverage.

Assessment

The Kenya-U.S. agreement is part of a wider policy shift by the U.S. and its partners into emerging critical mineral markets. Kenya’s deposits will remain important, but the agreement may represent something more significant: the growing competition for strategic resources. China’s dominance of the critical mineral market and the U.S. and partners' dependence have resulted in critical supply chains being increasingly viewed as strategic assets linked to industrial, economic, and national security.

China’s ability to implement export controls and subsequent entity listings has exposed some global vulnerabilities. Rather than solely resource-focused, Western countries have expanded supply chain concerns with refining and processing.

How effective these policies will be remains uncertain. However, the rapid policy shift and concerns from the West since Chinese restrictions in April 2025 suggest that critical minerals will likely continue to be a strategic resource, where leverage, sanctions, and restrictions converge.

What to watch.

The U.S. and partners' critical mineral agreements with emerging economies

Investment in refining and processing, as part of agreements with emerging economies, in the U.S. and Europe.

An expansion of Chinese export controls, restrictions, and entity listings.

Efforts to implement the G7 Critical Mineral Action Plan, including reducing dependence on a single supplier through diversification.

Kenya’s development of a processing industry through foreign investment.

Disruption in supply chains impacting the automotive, defence, tech, energy, and semiconductor industries.

Change in critical mineral production, global refining, and processing data, which may indicate how diversification or restrictions have impacted global markets.

Sources:

https://www.reuters.com/world/africa/kenya-us-close-critical-minerals-deal-ruto-says-2026-06-17/

https://www.ft.com/content/358f1fdc-d19b-4cdc-b1f9-84b9d2cabb3c?

https://pubs.usgs.gov/periodicals/mcs2026/mcs2026-rare-earths.pdf

https://www.iea.org/reports/rare-earth-elements/executive-summary

https://ec.europa.eu/commission/presscorner/detail/fr/statement_25_1552

https://www.csis.org/analysis/g7-critical-minerals-ambitions-and-irans-natural-resources